However, operating a compliant payroll for IT staff in Vietnam requires navigating a distinct set of regulatory obligations — from mandatory social insurance contributions to personal income tax withholding and a set of filing deadlines that run monthly and annually.

2026 brought two significant regulatory updates at the same time: a new minimum wage decree and the country’s most substantial personal income tax reform since 2012. Organizations that haven’t updated their payroll processes accordingly face meaningful compliance exposure.

This guide is written for HR leads, finance directors, and operations managers at foreign companies hiring IT talent in Vietnam. It covers the core payroll obligations, 2026 regulatory updates, the step-by-step payroll process, and the compliance options available to companies that have not yet established a local legal entity.

1. Why Vietnam Payroll in IT Requires a Dedicated Approach

Three concurrent obligations — all employer-managed

Vietnam’s payroll system places the employer at the center of three interlocking statutory obligations that run simultaneously from the date the first labor contract is signed:

- SHUI (Social Insurance, Health Insurance, Unemployment Insurance) — mandatory contributions calculated on gross salary, split between employer and employee, remitted monthly to Vietnam Social Security.

- Personal Income Tax (PIT) withholding — the employer is legally responsible for deducting PIT from employee salaries and filing declarations with the General Department of Taxation on a monthly or quarterly basis.

- Annual PIT finalization — a mandatory year-end reconciliation that the employer files on behalf of all employees by 31 March each year.

Organizations without prior experience in Vietnam frequently underestimate the interdependency of these three obligations. An error in SHUI calculation affects PIT taxable income. A misclassified allowance affects both. Managing them correctly requires either in-house expertise or a qualified local payroll provider.

Currency note: All salary payments must be made in Vietnamese Dong (VND). Foreign currency payment is only permissible for employees who are foreign nationals, and only when explicitly stated in their labor contract.

What does the IT talent cost structure look like in Vietnam in 2026?

Understanding the full cost structure — not just the gross salary — is essential for accurate headcount budgeting. The table below reflects current market rates for IT roles in major cities, based on Reco’s placement data:

Source: Reco internal placement data, 2025–2026. USD converted at approximately VND 25,400. Figures vary by specialization, seniority level, and location.

In addition to base salary, a standard IT compensation package in Vietnam typically includes structured allowances (meal, transport, phone/internet), a 13th-month salary paid ahead of Tet (market-standard in the IT sector, though not legally mandated), performance bonuses, and often supplementary private health insurance beyond the statutory BHYT coverage.

The structure of these components — not just the total value — affects both the employee’s net take-home pay and the employer’s total cost of employment.

Talent sourcing: Reco's RECO 7 model delivers shortlisted IT candidates within 7 business days, with compensation benchmarking included. Contact bd@reco-vn.com or visit RECO 7 for more2. How IT Payroll Differs from Standard Payroll in Vietnam

Generic payroll guides cover the statutory basics — minimum wage, SHUI rates, PIT brackets. For most industries, that is sufficient. IT is different. The way technology professionals are compensated, engaged, and managed creates a layer of payroll complexity that standard HR processes are not designed to handle.

Based on Reco’s experience managing payroll for IT teams across Vietnam, here are the five areas where IT payroll consistently requires a more specialized approach.

2.1. IT compensation packages have significantly more components

A developer’s monthly payroll calculation is rarely straightforward. A typical IT compensation structure can include:

- Basic salary

- Project-based bonus

- Performance bonus

- Overtime (including night deploys and weekend production support)

- Role-specific allowances (on-site, phone, internet, equipment)

- On-site allowance for client-facing or overseas-deployment roles

- Sprint or KPI-based incentives

- ESOP / equity components

- Signing bonus

Each of these components has a different tax treatment under Vietnamese PIT law. Some qualify as non-taxable allowances. Some are taxable in the period received. ESOP and equity income follow entirely separate rules. Misclassifying any component — or applying the wrong PIT treatment — creates reconciliation issues at year-end finalization and potential exposure during tax audits.

By contrast, payroll in retail, administration, or service industries typically involves a fixed salary, standard allowances, and sales-based incentives — a much simpler structure to administer.

Why this matters: Every compensation component needs to be correctly categorized before payroll runs. Getting this right from the start prevents costly reclassifications later.

2.2. IT organizations use a wider range of employment arrangements

IT companies routinely manage multiple engagement types simultaneously within the same team:

- Full-time employees under indefinite labor contracts

- Fixed-term contractors on project-based engagements

- Freelancers engaged under service contracts

- Remote employees working across multiple client locations

- Outsourcing staff embedded at client sites

- On-site staff deployed to overseas clients

Each arrangement carries different obligations: different contract structures, different tax withholding rules, different SHUI eligibility, and in some cases, different currencies and cross-border payment requirements.

A payroll system designed for standard office employment cannot reliably manage this mix. Foreign companies managing hybrid IT teams in Vietnam need a payroll provider that understands how each engagement type is treated under Vietnamese labor and tax law — and how to handle international payment flows where applicable.

Reco's Payroll service is built to handle the full range of IT employment arrangements — from full-time employees to contractor and on-site staff within a single managed framework.2.3. Payroll is tightly coupled with project and timesheet data

In most industries, payroll is an HR function. In IT companies, it is a cross-functional process. Monthly salary calculations frequently depend on inputs from multiple teams:

- Project Managers: billable hours, sprint completion, project allocation percentages

- Delivery teams: overtime triggered by production releases or deployment windows

- Accounting: cost allocation across client projects and internal budgets

- HR: leave balances, allowance eligibility, contract status

A developer working 50% on Project A and 50% on Project B, with overtime during a production release and a sprint-completion bonus, requires payroll data from at least three sources before a single calculation can begin. When this data arrives late, is inconsistent, or is formatted differently by each team, payroll cycles are delayed and errors compound.

IT payroll providers need established workflows for consolidating this data accurately and on time — not just the ability to run calculations once the data arrives.

2.4. Overtime in IT has distinct characteristics

Vietnamese labor law defines overtime as work beyond 48 hours per week, with statutory rates of 150% on regular days, 200% on rest days, and 300% on public holidays. For most industries, overtime is occasional and predictable.

IT operations follow a different pattern. Production deployments happen at night to minimize user impact. Critical bug fixes happen over weekends. System support during peak load events does not follow business hours. For IT teams, overtime is structural — built into the delivery model — rather than exceptional.

This means IT payroll must account for:

- On-call and standby allowances for system monitoring roles

- Night shift premiums for deployment and DevOps teams

- Weekend production support compensation

- Accurate timesheet integration to capture and verify these hours

Each of these has specific tax treatment implications. Correctly classifying and compensating IT-specific overtime — and ensuring it is reflected accurately in PIT calculations — requires payroll processes that go beyond standard overtime administration.

2.5. Higher salaries mean more complex tax positions

Vietnam’s PIT system is progressive. For most industries, where salaries sit in the lower brackets, PIT calculations are straightforward. IT salaries — particularly at senior and lead levels — regularly enter the upper brackets, where the tax position becomes more complex.

Several factors compound this complexity for IT professionals:

- ESOP and equity income: Taxed differently from salary income — typically as investment income or capital gains — requiring separate treatment in payroll and at annual finalization.

- Income from overseas sources: Developers working on international client projects, or receiving portions of their compensation from parent companies abroad, may have dual-source income that requires careful PIT residency analysis.

- Signing bonuses and irregular payments: Large one-off payments can push an employee into a higher effective bracket in the month they are received, requiring careful timing and structure.

- Year-end finalization complexity: Employees with multiple income sources, equity vesting events, or overseas income components require more detailed annual PIT finalization than standard employees.

For foreign companies managing senior IT talent in Vietnam, the risk of PIT errors is higher — and the financial exposure from those errors is proportionally larger.

3. Key Payroll Vietnam Regulations for 2026

Regional minimum wage: Decree 293/2025/NĐ-CP (effective 1 January 2026)

Decree 293/2025/NĐ-CP, issued on 10 November 2025, raised the regional minimum wage by an average of 7.2% across all four regions, effective 1 January 2026.

| Region | Key Areas | Monthly (VND) | Hourly (VND) |

| I | Hanoi, HCMC, Hai Phong, Da Nang | 5,310,000 | 25,500 |

| II | Binh Duong, Dong Nai, Can Tho | 4,730,000 | 22,700 |

| III | Hai Duong, Khanh Hoa, Long An | 4,140,000 | 19,900 |

| IV | Rural and less-industrialized areas | 3,700,000 | 17,800 |

For IT roles, market salaries are significantly above the minimum wage floor, so this update does not directly increase salary costs for technical staff. Its operational significance for foreign employers relates to three areas:

- SHUI calculation reference: The minimum wage anchors the cap for unemployment insurance contributions.

- Contract compliance: Any employee whose contracted salary was set at the 2025 minimum must have their contract formally updated via a signed addendum.

- Regional classification: The applicable wage region is determined by the physical location of the workplace, not the company’s registered headquarters. Remote IT staff working from different provinces may fall under a different regional tier.

SHUI contributions: employer cost structure

SHUI contributions represent the largest additional cost beyond gross salary. The employer’s portion (21.5%) is calculated on top of the gross salary and is not deducted from the employee’s pay.

| Insurance Type | Employer | Employee | Combined |

| Social Insurance (SI) | 17.5% | 8% | 25.5% |

| Health Insurance (HI) | 3% | 1.5% | 4.5% |

| Unemployment Insurance (UI) | 1% | 1% | 2% |

| TOTAL | 21.5% | 10.5% | 32% |

Source: Vietnam Social Insurance Law (effective July 2025)

For foreign (expat) employees, unemployment insurance does not apply, bringing the combined contribution rate to 30% (19.5% employer + 10.5% employee).

Contribution caps: Social Insurance and Health Insurance contributions are capped at 20 times the basic salary reference rate (currently VND 2,340,000/month), giving a monthly SI/HI cap of VND 46,800,000. Unemployment Insurance is capped at 20 times the applicable regional minimum wage. Contributions for senior IT staff earning above the SI/HI cap are therefore calculated against the capped figure, not the full salary.

A significant change from mid-2025: the expanded Social Insurance Law now mandates SHUI enrollment for any worker engaged under a labor contract of one month or more. This applies regardless of whether the role is full-time, part-time, or project-based, and directly affects how short-term IT project teams should be structured.

Payroll management: Reco’s Payroll service handles all SHUI registration, monthly contributions, and compliance reporting on behalf of client organizations — no in-house setup required. Learn more at reco-vn.com/payroll

Reco's Payroll service handles all SHUI registration, monthly contributions, and compliance reporting on behalf of client organizations — no in-house setup required. Learn more at Reco Payroll.Personal Income Tax: 2026 reform overview

PIT Law No. 109/2025/QH15, enacted on 10 December 2025, introduces the most significant reform to Vietnam’s personal income tax system since 2012. The changes directly affect how employer payroll systems calculate monthly withholding.

| Item | Before 2026 | From 2026 |

| Number of tax brackets | 7 | 5 (simplified) |

| Personal deduction | VND 11M/month | VND 15.5M/month |

| Dependent deduction | VND 4.4M/month | VND 6.2M/month |

| Top rate threshold | Above VND 80M/mo | Above VND 100M/mo |

| Tax rate range | 5% – 35% | 5% – 35% (unchanged) |

| Effective date (salaries) | — | Deductions: 1 Jan 2026 | 5-bracket: 1 Jul 2026 |

Important — effective dates and pending guidance: The increased deductions (VND 15.5M personal / VND 6.2M per dependent) apply from 1 January 2026. The 5-bracket progressive schedule officially takes effect from 1 July 2026. From January 2026, employers apply provisional PIT withholding using the new deduction levels. A Ministry of Finance Circular specifying the exact bracket thresholds is pending publication — payroll systems should be updated once this Circular is issued. In the meantime, organizations should confirm their calculation methodology with a qualified tax advisor.

The practical business impact: senior IT staff will see a higher net income at the same gross salary from mid-2026 onward, without any change to the employer’s cost. This is a talent retention benefit that organizations can communicate proactively during the hiring process.

Expat employees: Non-resident foreign employees pay a flat 20% PIT on Vietnam-sourced income, withheld at source. Vietnam has over 80 double taxation agreements — including with major source markets — that may reduce effective rates for qualifying individuals.

Action for payroll teams: If your payroll system has not yet been updated to reflect the 2026 deduction levels (VND 15.5M personal / VND 6.2M dependent), this should be prioritized immediately. Reco’s managed payroll service applies all regulatory updates automatically — reco-vn.com/payroll

4. The Payroll Process in Vietnam: Step by Step

Pre-payroll setup: mandatory registrations

Before the first payroll run, foreign entities must complete the following registrations within 30 days of signing their first labor contract:

- Social Insurance Unit Code: Register via the Vietnam Social Security (VSS) portal (Form TK3-TS) to activate SHUI coverage for employees.

- Employee tax codes: Each employee must have an individual PIT tax code registered with the General Department of Taxation before their first pay run.

- Corporate bank account registration: The company bank account must be linked to the tax authority. Mandatory for salary payments exceeding VND 5 million per transaction.

- Labor contract compliance: Contracts must be compliant with the Vietnamese Labour Code, including provisions on role, remuneration, working hours, probation, and termination.

No entity? Companies without a Vietnam-registered legal entity cannot complete these registrations independently. Reco’s EOR service provides a compliant alternative — acting as the legal employer on behalf of the client organization, with full operational readiness within 7 days. reco-vn.com/eor

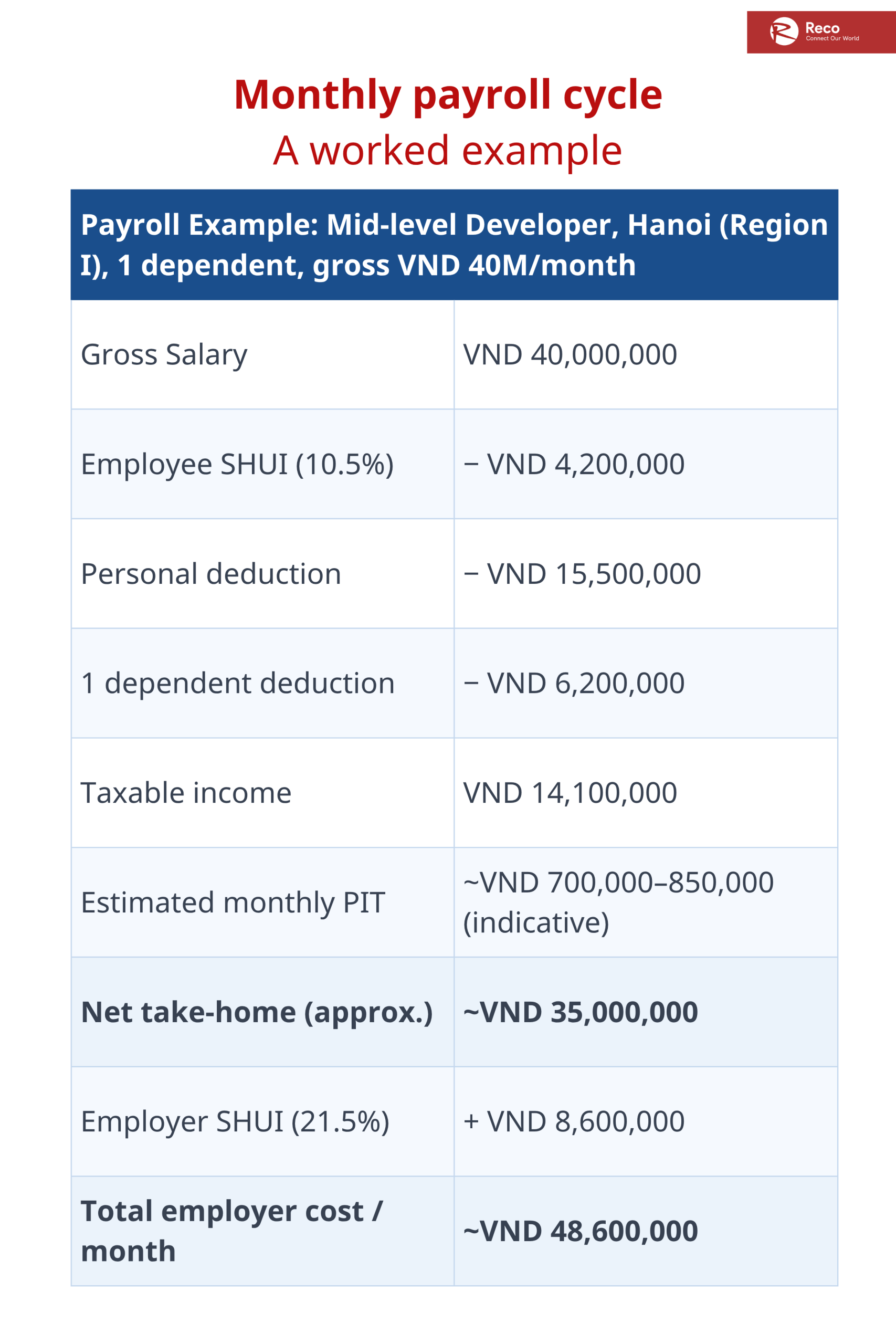

Monthly payroll cycle: a worked example

The following illustrates the standard monthly payroll calculation for a mid-level IT employee. The same methodology applies at all seniority levels — gross salary and PIT bracket change; the structure does not.

Note: PIT figure is indicative, calculated on the current 5% rate applicable to the taxable income level in this example. Exact bracket rates are subject to the forthcoming Ministry of Finance Circular. All calculations should be confirmed against official guidance.

The total employer cost of VND 48.6 million — not the VND 40 million gross — is the figure that should be reflected in headcount planning and budget allocation.

Read more: Top 7 Payroll Outsourcing Companies in Vietnam for Foreign BusinessesFiling deadlines

| Obligation | Frequency | Deadline |

| PIT declaration (monthly) | Monthly | 20th of the following month — companies with revenue > VND 50B/year |

| PIT declaration (quarterly) | Quarterly | Last day of month following the quarter — revenue ≤ VND 50B/year |

| SHUI remittance | Monthly | Last day of the current month |

| Annual PIT finalization | Annual | 31 March (employer filing on behalf of employees) |

| Individual self-finalization | Annual | 30 April of the following year |

Late filing penalties: PIT declaration delays attract administrative fines of up to VND 25 million per instance, plus 0.03% per day interest on outstanding amounts. For organizations managing teams of 20 or more, the cumulative exposure from a single missed deadline is material.

Never miss a deadline: Reco’s Payroll service manages the full monthly and annual filing cycle on behalf of client organizations — PIT declarations, SHUI remittance, and year-end finalization. reco-vn.com/payroll

5. Common Compliance Risks for Foreign IT Employers

Misclassifying employees as freelance contractors

This is the most common payroll compliance error made by foreign companies entering Vietnam. Engaging Vietnamese developers via international transfer as ‘contractors’ or ‘service providers’ to avoid SHUI and PIT obligations is a widely-used workaround — and one that carries significant legal exposure.

Under Vietnam’s expanded Social Insurance Law effective July 2025, any worker engaged under an employment-like arrangement — regular fixed remuneration, exclusive engagement, employer-directed work, employer-provided tools — is subject to mandatory SHUI enrollment. Misclassification exposes the engaging company to retroactive SHUI back-payments with penalties, administrative fines per affected worker, and complications if the arrangement is later formalized.

For senior IT staff on long-running engagements, the financial exposure from years of misclassification can be substantial.

Incorrect allowance structuring

Vietnam’s PIT framework distinguishes between taxable and non-taxable allowances. Meal, transport, and phone/internet allowances qualify for PIT exemption up to Ministry of Finance thresholds. Equipment allowances, when properly documented as business expenses, may also qualify. The 2026 PIT law expanded exempt categories further.

Defaulting to base salary for all compensation components inflates taxable income, increases PIT liability for the employee, and reduces the competitiveness of the package on a net-of-tax basis — without any change to the total employer cost.

Missing mandatory contract updates

Following Decree 293, any labor contract where the salary was set at or close to the 2025 minimum wage floor requires a signed addendum updating the figure. During labor authority audits, inspectors cross-reference the Enterprise Registration Certificate against payroll records and regional wage tiers. Discrepancies — even unintentional ones — produce audit findings.

Compliance review: If your organization has IT staff currently engaged in Vietnam — whether under formal contracts or informal arrangements — Reco can assess your current setup and recommend the most compliant path forward. Contact [email protected]

6. Payroll Compliance Without a Local Entity

The structural challenge for foreign companies

A common operational scenario for foreign companies expanding into Vietnam: IT candidates are identified, offers are ready to extend, but the legal entity establishment process is still underway — or the business case for a permanent entity hasn’t been confirmed.

Without a registered Vietnam entity, an organization cannot execute a compliant labor contract under Vietnamese Labour Code, register employees for SHUI, act as a PIT withholding agent, or maintain a local corporate bank account for payroll disbursement.

The result: the IT workforce operates outside the statutory employment framework, without formal SHUI protection, and the engaging organization carries undisclosed legal liability in the jurisdiction.

Employer of Record (EOR) as a compliant solution

An EOR provider acts as the legal employer on behalf of the client organization. The client retains day-to-day management of the IT team; the EOR manages all employment, payroll, and compliance obligations under Vietnamese law.

Under this model, the EOR executes labor contracts, registers SHUI, withholds and files PIT, disburses salaries, meets all statutory deadlines, and issues the client a single consolidated invoice. The arrangement is fully compliant and transparent, with no hidden obligations on the client side.

Read More: What is an Employer of Record? How EOR Works for Global HiringEOR is particularly relevant for organizations in the following situations:

- Market entry: Deploying a pilot IT team before committing to entity establishment.

- Project-based engagement: Fixed-scope IT work where long-term entity overhead is not justified.

- Speed-critical hiring: Where competitive talent windows do not permit a 2–4 month entity setup timeline.

- Regulated industries: Fintech, healthtech, and other sectors where informal engagement arrangements carry significant institutional risk.

Reco EOR — operational in 7 days: Reco acts as the legal employer for IT teams in Vietnam, covering labor contracts, SHUI, PIT, and monthly payroll. No local entity required. Operational within 7 days. Scalable as headcount grows. reco-vn.com/eor

Managed payroll vs. in-house HR: a framework for decision-making

| In-house HR Setup | Reco Managed Payroll / EOR | |

| Time to first payroll | 2–4 months | 7 days (Reco EOR) |

| Fixed overhead | HR salary + systems + training | Transparent per-head fee |

| Compliance risk | High without local expertise | Managed by specialists |

| Regulatory updates | Manual tracking required | Applied automatically |

| Reporting | Vietnamese (primarily) | English / bilingual (EN/JP) |

| Scalability | Tied to HR headcount | Flexible with team size |

For organizations with fewer than 50 IT staff in Vietnam, or those in active scaling phases, managed payroll consistently delivers a lower total cost of ownership when compliance risk is factored in. In-house capability becomes the appropriate investment once an organization has a stable local footprint and sufficient headcount to justify the fixed HR overhead.

7. About Reco — Vietnam IT Payroll & Workforce Solutions

Most foreign companies discover the complexity of Vietnam IT payroll the hard way — a missed SHUI deadline, a misclassified contractor, or a PIT calculation that does not survive year-end finalization.

Reco exists to prevent exactly that.

Since 2019, Reco has managed payroll and IT workforce solutions for 500+ clients across Asia — from two-person pilot squads to 100+ person offshore engineering centers — for organizations that needed compliance without the overhead of building it in-house.

Our Payroll and EOR services cover the full lifecycle: labor contracts, SHUI registration, monthly PIT withholding, filing deadlines, and bilingual reporting for your parent company. No local entity required. No compliance gaps. Operational within 7 days.

Beyond payroll, Reco’s RECO 7 headhunting model sources and shortlists qualified IT candidates within 7 business days — with compensation benchmarking built in. For organizations planning long-term, our BOT (Build-Operate-Transfer) model builds a dedicated offshore IT team in Vietnam and transfers full ownership to the client when ready.

330,000+ IT candidates · 500+ clients · 7+ years · Hanoi • Ho Chi Minh City • Tokyo

You focus on the product. We handle the compliance.

Looking to hire reliable and highly qualified tech professionals in Vietnam? Reach out to Reco Manpower today for tailored recruitment solutions that match your business needs.

FAQs

Engaging IT staff as freelance contractors rather than as employees under formal labor contracts. This arrangement — commonly used to avoid SHUI registration and PIT withholding — is non-compliant under Vietnam’s expanded Social Insurance Law (effective July 2025). Workers in ongoing, employer-directed engagements are classified as employees regardless of contract type. Misclassification exposes the organization to retroactive SHUI back-payments, administrative penalties per affected worker, and potential labor authority sanctions. The exposure compounds over time — organizations that have operated this way for multiple years can face substantial retroactive liability.

Yes — through an Employer of Record (EOR) arrangement. An EOR provider acts as the legal employer under Vietnamese law, executing labor contracts, registering employees for SHUI, managing PIT withholding and filing, and disbursing salaries. The client organization retains full management authority over the IT team’s day-to-day work. Reco’s EOR service can onboard a Vietnam IT team within 7 days, with no entity establishment required.

Reco produces bilingual payroll reports in English, structured to meet the governance and reporting requirements of foreign-invested enterprises (FDI). Reports cover individual payslips, SHUI contribution summaries, PIT withholding records, and monthly cost reconciliation. This reporting is designed to be compatible with parent company finance systems and allows finance and HR teams outside Vietnam to maintain full visibility of Vietnam payroll costs without requiring in-country expertise.